How NZ’s cost-of-living crunch compares with the UK, US, Australia and Canada – Inside Economics

Welcome to Inside Economics. Every week, I take a deeper dive into some of the more left-field economic news you may have missed. To sign up for my weekly newsletter, click here. If you have a burning question about the quirks or intricacies of economics send it to liam.dann@nzherald.co.nz or leave a message in the comments section.

Any winners in cost-of-living crisis?

Hi Liam,

I’d appreciate your expertise to understand the current cost-of-living issue that everyone is experiencing.

Is what NZers are experiencing the same in other countries, or have we got it worse (or better)?

Thanks!

Ren

A: Thanks, Ren.

It’s definitely worth doing a comparison with some of the major countries we like to compare ourselves to. I’ve picked Britain, the US, Canada and Australia.

My hunch before doing the research was that this is very much a global issue.

Covid stimulus, the Ukraine war, tariffs and this year, the Iran conflict, have conspired to make this an inflationary period.

That’s in stark contrast to the decade pre-Covid when inflation got so low we started talking about deflation and how central banks might need to take interest rates into negative territory to combat it.

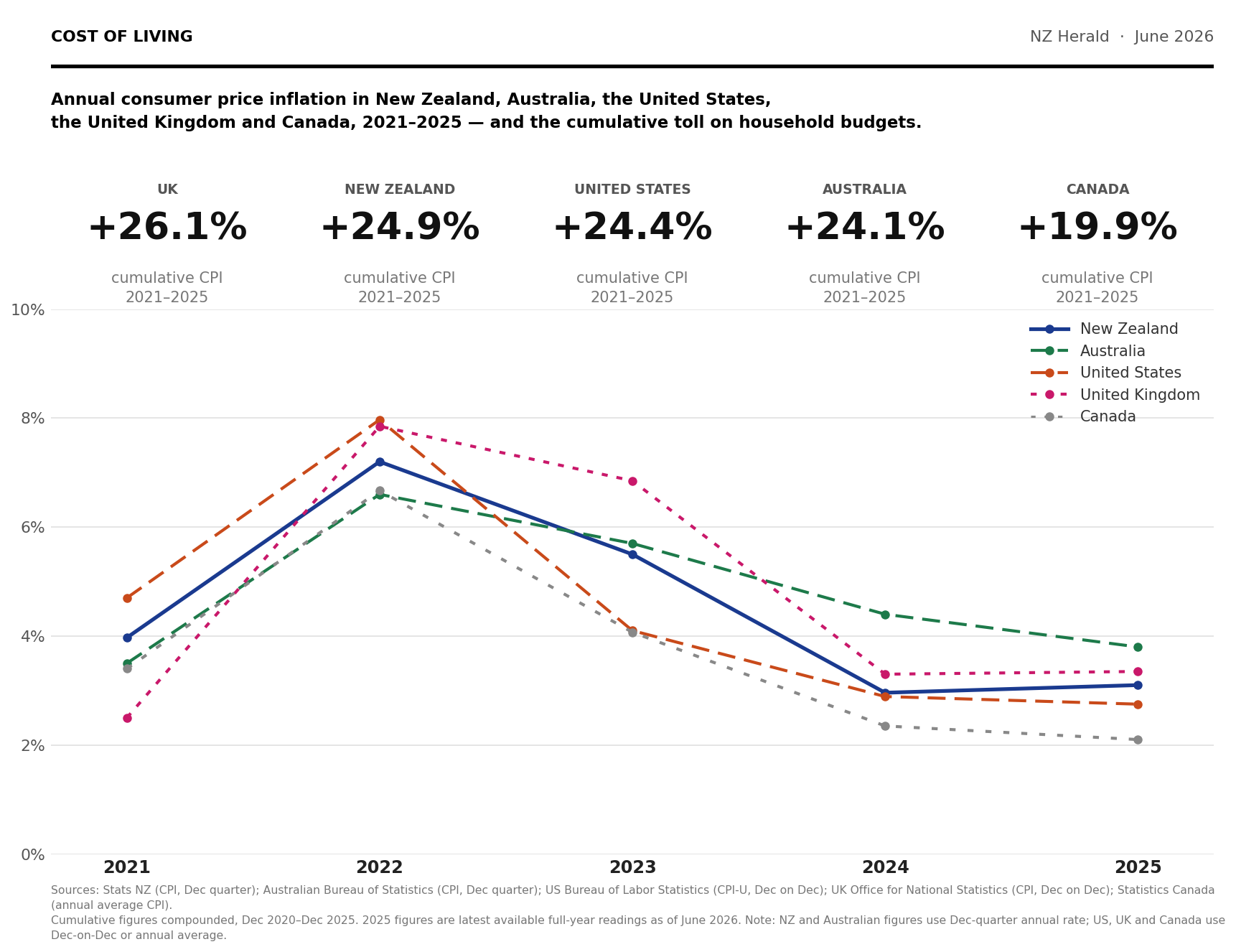

So let’s look back at cumulative Consumers Price Index (CPI) inflation across the past five years for all five countries:

Britain +26.1%, New Zealand +24.9%, United States +24.4%, Australia +24.1%, Canada +19.9%.

This is a fairly simple comparison, and it shows we are definitely not alone when it comes to the rise in goods and services.

We had the worst inflation rate in 2022, but we came down faster than Britain. Meanwhile, Australia has had worse inflation than us for the past year or so.

We’re sitting at a still elevated annual rate of 3.1% and Australia is at 4.6%.

Essentially, though, we’re all in the same ballpark.

What about the workers?

Of course, CPI is just one side of the equation.

When it comes to purchasing power, the extent to which wage inflation keeps up with the CPI inflation has a big impact on how much poorer a nation feels.

On that front, New Zealand doesn’t fare so well.

I should admit that my research gets a bit looser here. There are all sorts of different measures for wage inflation.

Even in New Zealand, we have the Labour Cost Index and the Quarterly Employment Survey.

The former measures the fixed cost of labour for employers, and the latter is a broader measure that includes actual earnings and is affected by compositional changes, ie, if more people move into higher-paid jobs, or overtime increases, average earnings go up even if no individual got a pay rise.

Anyway, the rankings look a bit different when you factor in wage inflation.

Canada and the US look the best with a marginal net positive (1%) gain in the cost of living.

Britain comes out flat, while Australia and New Zealand suddenly look a lot worse – going backwards by 6.6% and 7.7% respectively.

On that basis, it seems New Zealand has fared worse than other countries.

All those gripes about rising power prices, increasing council rates, meat and dairy are grounded in reality.

I would add, though, this calculation flatters things a bit for the countries that appear to have kept up.

For example, Britain, with the highest rate of inflation in the past five years, has been in a wage-price spiral. That’s still a bad thing.

So some workers have been able to demand higher wage increases to keep up.

But you can bet that hasn’t been the case for all workers. Also, those on fixed incomes, such as pensioners and beneficiaries, will be feeling the pain.

Winners and losers

Are there any winners from all this inflation? In theory, no. If big corporations are just passing on the cost increases, then they shouldn’t be making bigger profits.

But many are suspicious that higher price inflation gives companies cover to increase their margins.

This has been dubbed “greedflation”. The evidence for greedflation is mixed.

In New Zealand, the Commerce Commission has just released a Grocery Report that found the big companies’ margins have remained stable.

Although it is worth noting that they see profitability of local supermarket chains sitting at the top of the OECD, above Woolworths in Australia and Tesco in Britain.

The other winner is the Government, which quietly reaps the windfall from inflation, pushing people into higher tax brackets. This is dubbed fiscal creep.

The losers are basically anyone unable to raise prices or demand higher wages despite inflation.

I suspect it has hit the hospitality sector hard because eating and drinking out is discretionary. They can’t push prices up too much without losing customers.

It’s a trap that has seen many, much-loved cafes, bars and restaurants close in the past year (RIP Verona).

The solution

As we’ve both mentioned, just raising wages is no solution, as it creates an inflationary spiral.

So the primary solution for inflation is to reduce the money supply and, in turn, reduce demand in the economy. This is old-school monetarist policy.

Central banks lift interest rates to do just that. It is brutal, but it works.

It worked in the 1990s. It worked again after Covid. It will likely work again as rates rise later this year.

But I would add that we’ve faced a run of supply shocks in the past five years.

Central banks can respond to those, but they can’t control them.

I’m not sure how we solve that. Humans could stop going to war. That would be a good start.

Oil, inflation and the OCR

Q: What does this oil price drop mean for Official Cash Rate (OCR) forecasts, which play a more important role in our economic recovery?

We don’t need high interest rates again. Some banks have seven to eight future forecast increases, hence the longer-term interest rate is so high. Start pressing them why.

Kiwibank and ANZ economists have differing views. Is it because costs have been increasing because of the increase in oil prices, hence inflationary?

Now the banks will say oil prices are coming down so consumers will have more money to spend so this can be inflationary! We cannot win. One thing that is for sure is that bank profits will stay high.

Keep up the good work.

Kind regards,

Tim

A: Cheers, Tim.

I touched on this last week on the Economy of Everything podcast.

But given the pace at which the Iran-US conflict is moving, it is worth revisiting.

The peace talks don’t appear to have gone hugely well in the past week, but oil prices are still about US$80 ($140) a barrel, and pump prices here have dropped below $3 a litre.

As the CEO of Z Energy told me, we can’t expect the market to return to normal in a hurry.

The reserve supply of oil held by big nations such as China and the US has dropped dramatically to multi-decade lows.

So I don’t think we should expect prices to drop to the pre-war lows of US$63 per barrel.

But regardless, I think we’re going to see a stimulatory bump from lower petrol prices.

There’s probably $20 or $30 worth of weekly fuel costs going back into people’s pockets.

What does that do to the Reserve Bank’s equations?

I think you are right. Either way, we are looking at a rising OCR in coming months.

The inflationary damage done by the war is still flowing through the supply chain.

Economists expect we’ll see that push the CPI inflation rate above 4% this quarter.

Meanwhile, lower fuel prices should help bring inflation back down in the medium term. But in the short term, they may stimulate more spending activity in the economy. That is also inflationary to some extent.

We shouldn’t be afraid of economic growth.

I think the net result of the Iran conflict being resolved (touch wood) has to be good.

More than anything, it should remove uncertainty from the minds of businesses and consumers and boost confidence.

We should also bear in mind that the current OCR setting is lower than neutral. In other words, it is set to stimulate a recessionary economy.

That’s why many economists believe the RBNZ needs to move it from 2.25% to 2.75% or 3% in the next few months.

At that point, it will be set at neutral for an economy with low but steady growth.

I’d love to see the global situation get so boring that we could sit with those kinds of policy and monetary conditions for a year or so.

Credit crunch

Q: There is a strange attitude in the New Zealand bureaucratic psyche that while we look favourably and brag about the success of our co-operatives in sectors as diverse as agriculture, retail and healthcare, we seem to find small community-based financial services in suburbs, towns and regional locations beyond the pale and need to regulate them out of existence. Why?

A: Thanks, Rob.

Let me provide some context around this question.

Over the past few weeks, this column has run a lively discussion about the inequity of credit.

The richer you are, the more able you are to borrow at low rates of interest. The poorer you are, the more it costs to borrow.

I asked readers for solutions to the problem on the back of an envelope.

Rob came through with what he himself describes as an “A3-sized” back-of-the-envelope response.

I’ve posted the question part above, but while I can’t run it all, I’ll also paraphrase some of his main points.

Rob argues that for most of New Zealand’s history, ordinary Kiwis had access to affordable, community-based financial services through Trustee Savings Banks and the Post Office Savings Bank, until they were sold off in the privatisation wave of the 1980s (and 1990s).

Credit unions and building societies filled the gaps, operating as member-owned co-operatives with a 150-year international track record and not a single member ever losing a dollar.

He suggests the post-GFC regulatory response applied a one-size-fits-all framework that made no distinction between credit unions and building societies and the finance companies that actually failed.

That’s meant the credit union and building society model sector has been effectively regulated out of existence, leaving lower-income New Zealanders without access to fair credit, he says.

That, he argues, has fuelled the rise of buy now, pay later and predatory lending.

It’s an interesting point.

I’m not sure we can just blame regulation for the demise of co-operative lenders.

The tougher regulatory environment after the finance company collapses was very broad, sweeping up all non-bank lenders.

In the early 1980s, there were hundreds of credit unions in New Zealand.

Now, as far as I can see, there are just three: First Credit Union, Unity Credit Union, and Police and Families Credit Union. It’s a similar story for building societies.

But I think the big crunch in the industry predates the GFC.

That suggests it has more to do with the arrival of foreign banks and the rapid expansion of credit availability in the 1990s.

Pre-1987 deregulation, banks in New Zealand were tightly constrained – credit rationing was real, interest rates were controlled, and getting a mortgage or a personal loan from a bank was genuinely difficult.

When we sold our domestically owned banks, we deregulated the sector and also introduced lenders with much deeper pockets into the mix.

Suddenly, borrowing for houses was relatively cheap and easy.

House prices weren’t crazy yet and banks were happy with 10% deposits.

It’s no coincidence this is also when the housing market started to take off.

But times change. Lending restrictions are tough, and banks are more cautious.

Perhaps there’s still a place for co-operative lenders.

Don’t forget to check out the Herald’s new podcast, The Economy of Everything, with Liam Dann and Tamsyn Parker – thanks to CMC Markets.

Liam Dann is business editor-at-large for the New Zealand Herald. He is a senior writer and columnist, and also presents and produces videos and podcasts.

He joined the Herald in 2003. To sign up to his weekly newsletter, click on your user profile at nzherald.co.nz and select “My newsletters”.

For a step-by-step guide, click here. If you have a burning question about the quirks or intricacies of economics send it to liam.dann@nzherald.co.nz or leave a message in the comments section.