Reserve Bank’s Paul Conway: Higher inflation expectations could make price pressures stick

Reserve Bank chief economist Paul Conway is laser-focused on ensuring people don’t start expecting inflation to be above target in the future.

If they do, he fears businesses could hike prices too much, causing a bigger inflationary problem that is painful to get on top of.

Conway is particularly interested in inflation expectations in the current environment because the cost of living is front of mind for people.

“Our research finds that households and businesses pay more attention to inflation when it is above our 1 to 3% target range,” he said in a speech at a BusinessNZ event on Tuesday morning.

“With inflation having been above our target range for 14 of the 25 quarters since 2020, I’m pretty sure people are paying close attention to it now.

“If people place greater weight on elevated inflation in their decisions, the risk of a temporary cost shock becoming more persistent increases.”

Conway’s remarks came almost a week after the Monetary Policy Committee, which he is a member of, lifted the Official Cash Rate (OCR) for the first time in three years to 2.5%.

While some observers opposed the committee’s decision to remove some stimulus from the economy at a time it is still fragile, the move was supported by all committee members and aligned with what the market expected.

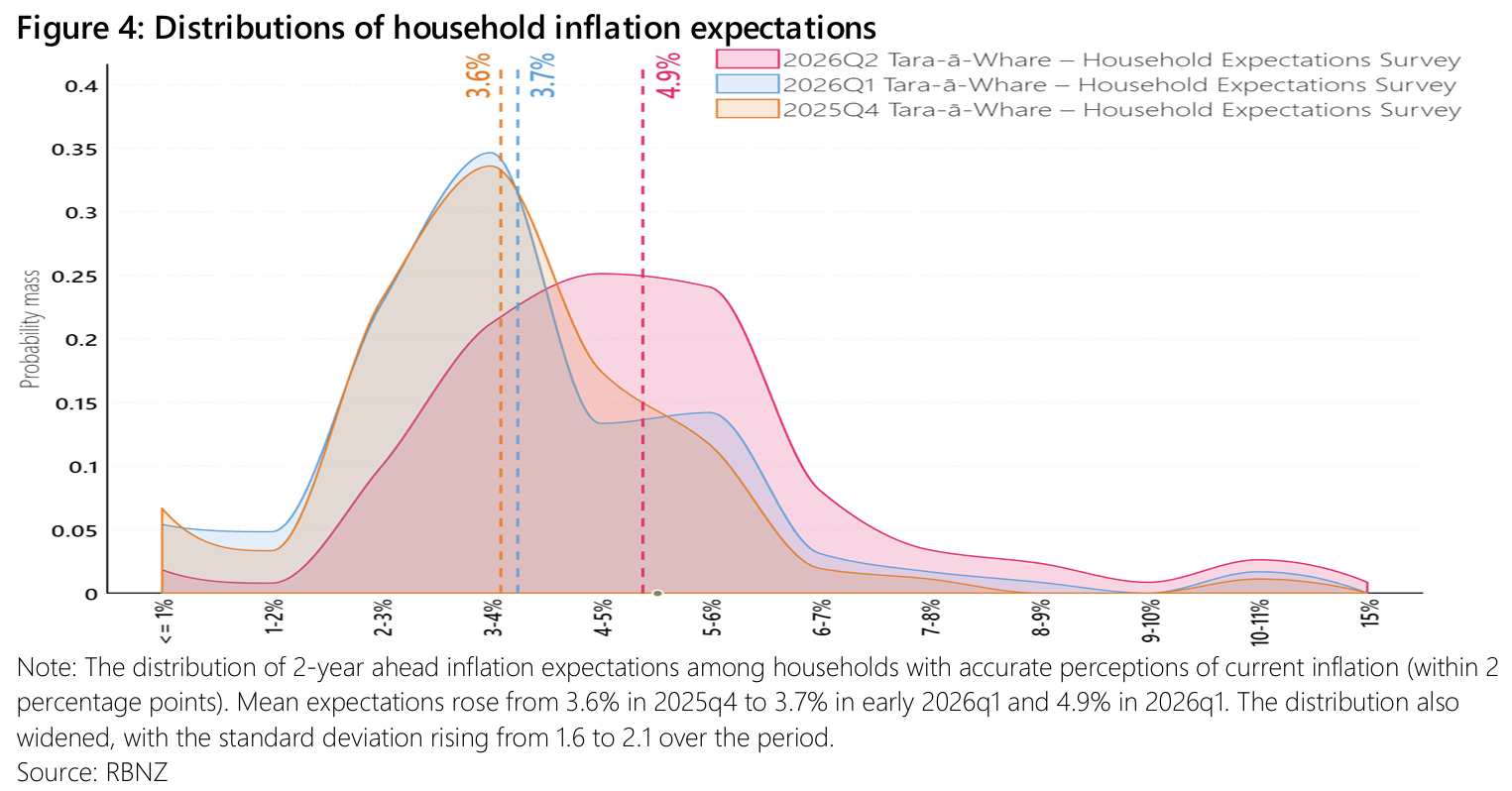

In his speech, Conway recognised households and small businesses typically had higher and more volatile inflation expectations than big businesses and professional forecasters.

However, the Reserve Bank found that households with more accurate perceptions of current inflation tended to better predict future inflation.

Zeroing in on these savvy households’ responses to the Reserve Bank’s surveys of inflation expectations, Conway noted that even their expectations for inflation two years ahead had increased and become more dispersed since the onset of the Middle East conflict.

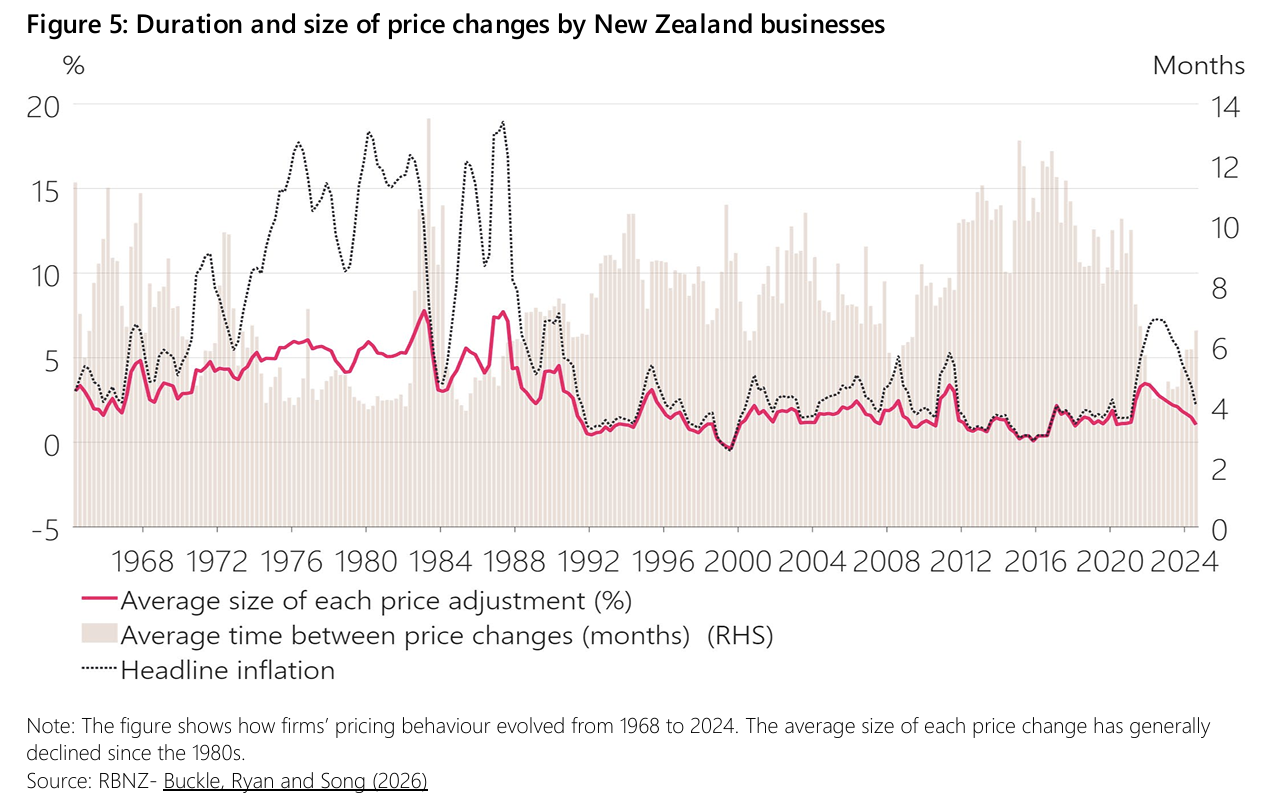

This was something he was paying attention to, as he noted larger firms were adjusting their prices more frequently, but by smaller amounts, than in the past.

“Essentially, advances in digital technology have made it cheaper and easier for firms to review and change prices, allowing them to respond more quickly to shifts in inflation expectations, actual costs and broader economic conditions,” he said.

“Larger firms tend to reprice more frequently, meaning that their pricing decisions can provide an early signal on inflation pressures in the economy.”

Conway noted New Zealand businesses had also become more likely to increase prices when costs increased, and less likely to cut them when they fell.

“Price-setting has become more asymmetric, with firms quicker to pass through rising costs than to reverse price increases as inflation recedes,” he said, noting this pattern was most evident among firms in the services sector.

Conway said pricing decisions were shaped less by the number of competitors firms had and more by the prices those competitors charged and the willingness of their customers to shop around.

“Taken together, these findings suggest that cost shocks may now pass through and become embedded in inflation more quickly than in the past,” Conway said.

“This reinforces the importance of keeping inflation expectations anchored and closely monitoring price-setting behaviour.”

This said, Conway acknowledged the inflation rate was also influenced by council rates and other prices controlled by central government.

These “administered prices” made a 0.7 percentage point contribution to the 3.1% increase in the Consumers Price Index in the year to the March quarter.

Concluding his speech, Conway said the Reserve Bank expected inflation to fall within its target range within the next year – largely because the sluggish economy (or all the spare capacity in the economy) was making it too difficult for firms to pass on cost increases.

He was encouraged that medium-term inflation expectations were “well anchored”.

“But after a prolonged period of above-target inflation, anchored inflation expectations cannot be taken for granted,” he said.

“If inflation pressures stemming from the Middle East conflict prove to be more persistent than expected, we will respond. Because when expectations become embedded in price-setting behaviour, bringing inflation back to target becomes much more difficult and costly.”

Jenée Tibshraeny is the Herald’s Wellington business editor, based in the parliamentary press gallery. She specialises in government and Reserve Bank policymaking, economics and banking.